A comprehensive guide to strategic asset allocation, risk management, and tactical rebalancing for the modern investor seeking sustainable growth

This article provides a deep dive into the mechanics of constructing a robust investment portfolio tailored for a twelve-month horizon. We explore the synergy between traditional assets and modern alternatives, the psychological discipline required for market volatility, and the technical frameworks used by professionals to hedge against inflation while capturing emerging market opportunities.

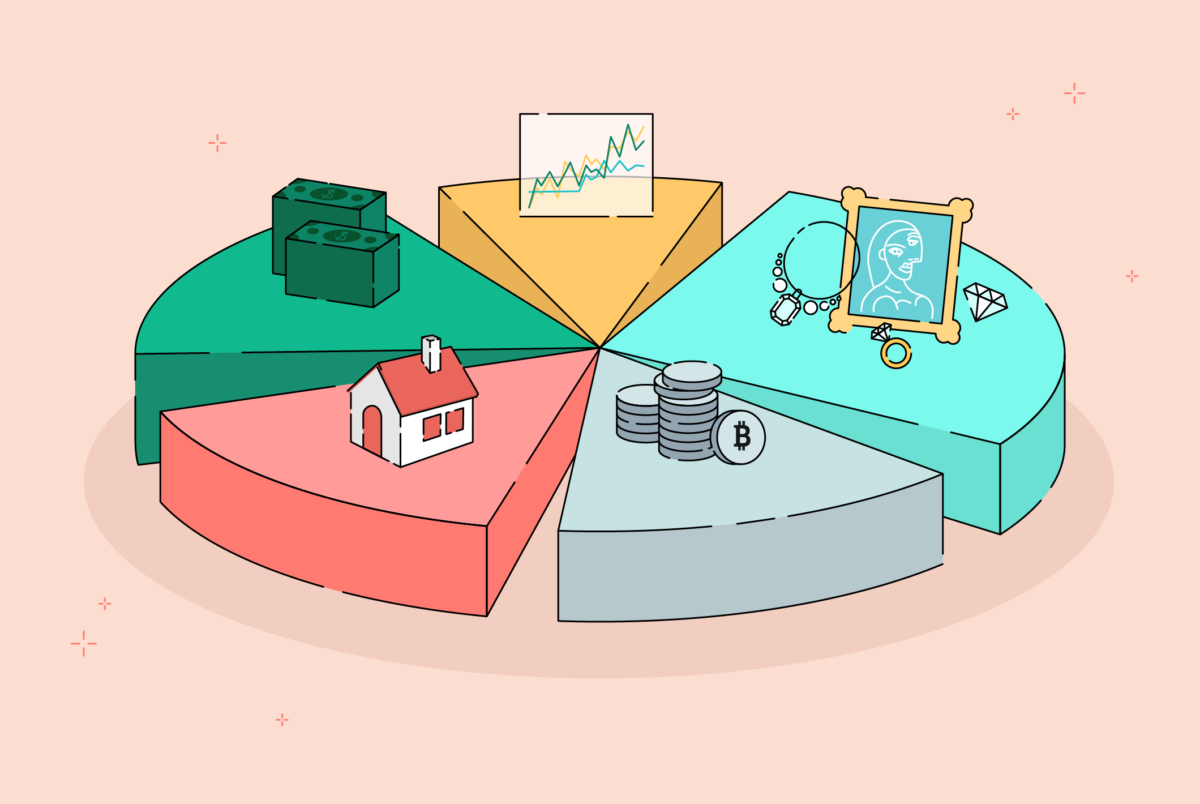

Constructing a successful investment portfolio for the year begins with a clear understanding of one’s financial objectives and risk tolerance. Strategic asset allocation is the process of dividing your capital among different asset classes, such as equities, fixed income, and commodities, to balance potential returns against the likelihood of loss. This initial stage is not about picking individual “winners” but about creating a structural framework that can withstand various economic cycles. Investors must assess the current macroeconomic climate, including interest rate trends and geopolitical stability, to determine whether a defensive, neutral, or aggressive stance is appropriate for the upcoming four quarters.

Building a portfolio requires a level of calculated risk and a deep understanding of probability, much like the strategic environment found in a casino. However, unlike house-based gaming, the financial markets allow investors to tilt the odds in their favor through diversification and long-term analysis. By moving away from pure speculation and focusing on evidence-based investing, an individual can transform their capital into a working engine of growth. The goal in the first month is to establish a core position that serves as an anchor, ensuring that even if certain sectors underperform, the overall integrity of the wealth-building strategy remains intact and functional.

Navigating the Equity Landscape for Growth

Equities remain the primary driver of capital appreciation for most portfolios, but the approach to stock selection must be nuanced in a one-year window. Investors should distinguish between value stocks, which are often undervalued by the market, and growth stocks, which represent companies expected to expand at an above-average rate. A balanced portfolio often utilizes a “core and satellite” approach, where the majority of equity exposure is held in broad-market index funds, while smaller, tactical positions are taken in specific sectors like technology or healthcare. This method captures the general upward trajectory of the market while allowing for outsized gains from high-performing industries.

The current year demands a particular focus on quality and earnings stability, as market volatility can quickly erode gains in speculative small-cap stocks. Analyzing debt-to-equity ratios and free cash flow is essential for identifying companies that can survive a potential downturn. Furthermore, geographic diversification within the equity sleeve is vital; relying solely on domestic markets exposes the investor to localized economic shocks. By including international developed and emerging markets, you create a global safety net that captures growth in different time zones and regulatory environments, ensuring your equity engine never fully stalls.

Fixed Income as a Volatility Buffer

Fixed income, traditionally comprising government and corporate bonds, serves as the essential ballast for any investment ship during stormy market weather. In a one-year investment plan, the role of bonds is primarily to provide liquidity and reduce the overall “beta” or volatility of the portfolio. When stock markets experience a correction, high-quality bonds often move in the opposite direction or at least hold their value, providing the investor with a psychological and financial cushion. Understanding the inverse relationship between bond prices and interest rates is crucial for timing these entries and managing the duration of the holdings.

Beyond simple government treasuries, investors can look toward inflation-protected securities to ensure that their purchasing power is not eroded by rising consumer prices. Corporate bonds offer higher yields but come with credit risk, making it necessary to stick to investment-grade issuers for a one-year horizon. The fixed income portion of the portfolio should be viewed as the “insurance policy” that pays a small dividend. By carefully laddering maturities—choosing bonds that expire at different times throughout the year—investors can ensure a steady stream of cash flow that can be reinvested or used for immediate financial needs without selling assets at a loss.

The Rising Importance of Alternative Assets

In the modern financial era, traditional stock-and-bond models are often supplemented with alternative assets to enhance diversification. Alternatives include real estate, private equity, precious metals, and even digital assets, which often have a low correlation with the broader stock market. For a one-year portfolio, including a small percentage of gold or silver can act as a hedge against currency devaluation and systemic banking risks. These assets do not produce cash flow, but their historical role as a store of value makes them indispensable during periods of high inflation or extreme geopolitical tension.

Real Estate Investment Trusts (REITs) provide another avenue for diversification, allowing investors to gain exposure to commercial or residential property markets without the hassle of physical management. These instruments often provide high dividend yields, making them attractive for income-focused portfolios. However, alternatives should be handled with caution, as they can be less liquid than public stocks. The key is to limit these holdings to a tactical “satellite” portion of the portfolio, ensuring they provide a unique return profile that offsets losses in traditional sectors during unconventional market events.

Psychological Discipline and Market Sentiment

One of the most overlooked components of portfolio management is the investor’s own psychology and their ability to stick to a plan when headlines turn negative. The “year-ahead” outlook is often clouded by “noise”—short-term news cycles that trigger emotional reactions like fear or greed. Professional investors use systematic rules to govern their behavior, ensuring they do not sell during a temporary dip or overextend themselves during a market bubble. Maintaining a professional detachment from daily price movements is what separates those who achieve annual targets from those who fall victim to market cycles.

Market sentiment often moves in extremes, and being a “contrarian” can sometimes be the most profitable path. This involves buying when others are fearful and trimming positions when the market becomes irrationally exuberant. However, for a standard one-year portfolio, the best psychological tool is the pre-determined exit strategy. By setting “stop-loss” orders or “take-profit” targets at the beginning of the year, you remove the burden of decision-making during high-stress moments. This clinical approach ensures that the portfolio remains a reflection of logic rather than a reaction to the chaotic collective emotions of the trading floor.

Taxation and Fee Optimization Strategies

An investment portfolio’s “gross return” is often a vanity metric; what truly matters is the “net return” after taxes and management fees have been deducted. High turnover within a portfolio can lead to significant capital gains taxes, which can eat away at a large portion of the year’s profits. Investors should prioritize tax-efficient vehicles such as exchange-traded funds (ETFs) over actively managed mutual funds, as ETFs generally trigger fewer taxable events. Additionally, holding assets for longer than a year where possible can shift the tax burden from short-term to long-term rates, which are typically much lower.

Management fees and brokerage commissions are the “silent killers” of wealth accumulation. Even a seemingly small fee of one percent can significantly compound over time, reducing the total value of the portfolio by thousands of dollars. Strategic investors seek out low-cost providers and focus on passive index funds that offer broad exposure for a fraction of the cost of active management. By auditing your portfolio for hidden costs and choosing tax-advantaged accounts when applicable, you effectively give yourself an immediate “raise” in performance that requires zero additional market risk.

The Role of Cash and Liquidity Management

Maintaining a portion of the portfolio in cash or cash equivalents is a strategic necessity, not a sign of indecision. Liquidity allows an investor to take advantage of “flash crashes” or sudden market opportunities that arise throughout the year. If a portfolio is one hundred percent invested, the investor is forced to sell an existing position—possibly at an inopportune time—to fund a new opportunity. A cash reserve of five to ten percent provides the “dry powder” needed to be opportunistic while also serving as an emergency fund for unforeseen personal expenses.

In a high-interest-rate environment, cash is no longer a “dead” asset; high-yield savings accounts and money market funds can provide respectable returns with zero risk to the principal. This “cash sleeve” acts as a volatility dampener, reducing the overall swing of the portfolio value. During the middle of the year, if the market becomes overvalued, increasing the cash position can be a prudent way to “lock in” gains. Liquidity management is the art of staying flexible, ensuring that you are never a “forced seller” and always have the capacity to act when the market offers assets at a significant discount.

Tactical Rebalancing and Portfolio Hygiene

A portfolio that starts the year perfectly balanced will inevitably become skewed as some assets grow faster than others. Tactical rebalancing is the process of selling a portion of your overperforming assets and buying more of your underperforming ones to return to your original target allocation. This forced “buy low, sell high” mechanism is one of the few ways to systematically improve risk-adjusted returns without needing to predict the future. Rebalancing should be done at set intervals, such as semi-annually or quarterly, to prevent transaction costs from becoming excessive.

Portfolio hygiene also involves cutting “dead wood”—investments that no longer fit the original thesis. If a company’s fundamentals have fundamentally shifted or a sector faces permanent structural decline, it is better to take a small loss early than to hold on in hope of a recovery that may never come. This disciplined pruning ensures that the portfolio remains lean and focused on high-probability outcomes. By treating the portfolio as a living organism that requires regular maintenance, the investor ensures that the capital is always allocated to its highest and best use throughout the calendar year.

Monitoring Macro Trends and Geopolitical Risks

While a portfolio is built on micro-decisions, it exists within a macro environment that can be shifted by major global events. Investors must stay informed about central bank policies, particularly the actions of the Federal Reserve, as interest rate changes ripple through every asset class. Inflation data, employment reports, and manufacturing indices are the “vital signs” of the economy that dictate whether a portfolio should lean toward cyclical stocks or defensive utilities. A sudden shift in trade policy or a conflict in a major oil-producing region can rapidly change the risk profile of international holdings.

Risk management involves not just looking for profit, but identifying “tail risks”—unlikely but catastrophic events that could derail a portfolio. Hedging strategies, such as buying “put options” or increasing exposure to non-correlated assets like commodities, can protect against these outliers. It is important to remember that the market often “prices in” known risks, so the real danger usually comes from the “unknown unknowns.” By maintaining a global perspective and staying humble about one’s ability to predict the news, an investor builds a resilient structure that prioritizes survival over ego, ensuring they are still in the game for the following year.

Conclusion

Building an investment portfolio for the year is a process that blends the precision of mathematics with the discipline of professional management. It is an exercise in preparation, requiring the investor to look past the noise of the present and focus on the structural drivers of wealth. From the foundational importance of asset allocation to the tactical execution of rebalancing and fee optimization, every decision must serve the twin goals of capital preservation and growth. Success is not defined by a single lucky trade, but by the cumulative effect of a well-executed plan that accounts for both the expected and the extraordinary.

As you look toward the final months of your annual cycle, the focus should shift from accumulation to evaluation. Reflecting on which strategies worked and which failed provides the essential data needed to refine the plan for the following year. Investing is a lifelong journey of learning and adaptation; the portfolio you build today is a stepping stone to the financial freedom of tomorrow. Stay disciplined, keep your costs low, and never underestimate the power of a diversified approach.